search

date/time

Wed, 1:00AM

overcast clouds

7.6°C

NE 8mph

overcast clouds

7.6°C

NE 8mph

| Sunrise | 4:26AM |

| Sunset | 7:49PM |  |

P.ublished 1st May 2026

business

IoD: Business Confidence Lifts But Supply Chain Concerns Rise

Business leader confidence in their own organisations also rose, to +8 in April from -2 in March.

Cost expectations fell to +85 from +88

Investment intentions rose to -9 from -13 (investment intentions have been net negative every month since August 2024)

Revenue expectations rose to +17 from +13

Export expectations were broadly unchanged at +3 from +2 in March

Headcount expectations dropped to -3 from 0

1 in 5 (20%) stated that their organisations had already experienced shortages as a result of the conflict in the Middle East, of which a third (32%) judged them significant

Amongst those who reported shortages, 55% had experienced shortages in fuel or energy, 38% in industrial materials and 34% in components or parts

Meanwhile, over half (52%) are worried about shortages impacting their business in the coming months, with 76% concerned about fuel or energy, 35% components or parts and 34% industrial materials

At present, only 37% have taken, or are planning to take, action to mitigate the impact of shortages on their business – with the most significant action being increased awareness of supply chains (25%), improved relationships with key suppliers (19%) and diversification of suppliers across a broader range of countries (18%)

As the conflict in Iran continues, there are growing concerns among firms over potential shortages, particularly amongst those with complex physical supply chains. Around a third of manufacturers, wholesalers/retailers and construction companies have already experienced shortages. And you can see firms are taking clear steps to better manage risk to their supply chains, through investing time in improving relationships with key suppliers, better understanding vulnerabilities in supply chains, diversification and stockpiling.

Amidst yet another global shock, there’s a distinct sense from business leaders that navigating global uncertainty is becoming normalised in board rooms. April has seen a small improvement in the confidence of business leaders in the economic outlook, accompanied by rises in revenue expectations and investment plans. Although these improvements are from very low bases, there is more evidence of targeted investment resuming, particularly in AI, with growth opportunities in renewables and international markets. But the dominant theme is of ongoing cost pressure, regulatory burdens, fragile demand and hiring freezes.

As firms take actions to address their own resilience and supply security, it is important for the UK to do the same. Increased access to international markets – including the EU – will improve the UK’s growth resilience over time. But urgent action is needed to address UK energy costs. There must be an honest recognition that the UK will remain reliant on fossil fuels for many years to come, even while we push hard for the important shift to renewables. It makes sense to exploit and monetise our own resources, for the UK’s economic security.

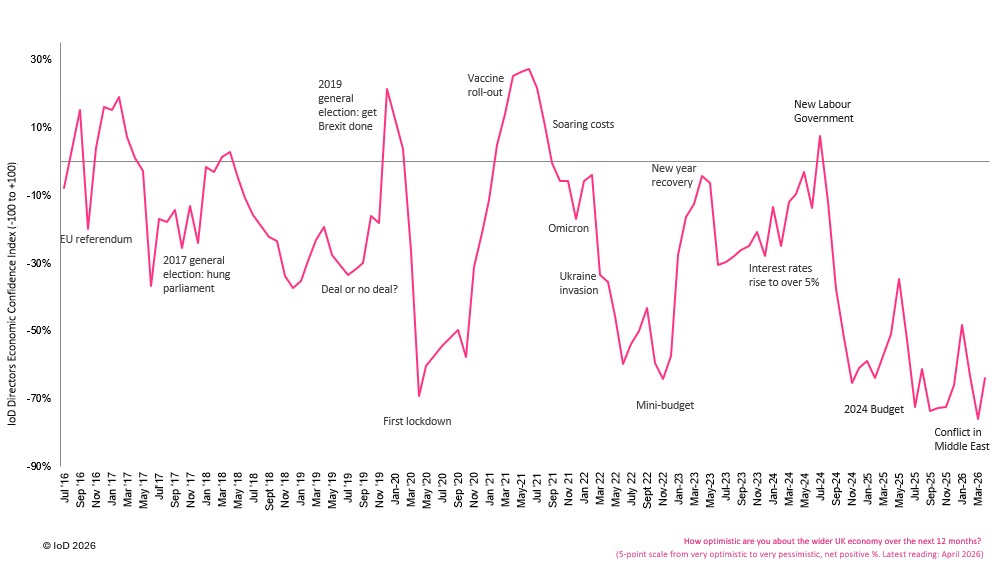

The IoD Directors’ Economic Confidence Index measures the net % positive answers from members of the Institute of Directors to the question ‘How optimistic are you about the wider UK economy over the next 12 months?’ on a five-point scale from ‘very optimistic’ to ‘very pessimistic’.

Full Results

900 responses from across the UK, conducted between 16-30 April 2026. 18% ran large businesses (250+ people), 18% medium (50-249), 21% small (10-49 people), 31% micro (2-9 people) and 12% sole trader and self-employed business entities (0-1 people).

How optimistic are you about both the wider UK economy and also your organisation over the next 12 months?

| Very optimistic | Quite optimistic | Neither optimistic nor pessimistic | Quite pessimistic | Very pessimistic | Don't know | |

| Wider UK economy | 0.4% | 9.2% | 16.7% | 48.9% | 24.7% | 0.1% |

| Your (primary) organisation | 3.7% | 32.6% | 34.9% | 22.4% | 6.0% | 0.4% |

Comparing the next 12 months with the last 12 months, what do you believe the outlook for your organisation will be in terms of:

| Much higher | Somewhat higher | No change | Somewhat lower | Much lower | N/A | Don't know | |

| Business investment | 3.0% | 23.1% | 36.9% | 22.2% | 12.7% | 1.4% | 0.7% |

| Costs | 20.4% | 67.3% | 8.4% | 1.9% | 0.8% | 0.6% | 0.6% |

| Exports | 2.7% | 13.7% | 31.1% | 9.4% | 4.1% | 36.7% | 2.3% |

| Headcount | 1.2% | 24.4% | 43.2% | 21.2% | 7.1% | 2.2% | 0.6% |

| Revenue | 5.2% | 41.7% | 21.7% | 23.6% | 6.3% | 1.0% | 0.6% |

| Wages | 3.9% | 42.4% | 40.0% | 8.6% | 2.4% | 1.9% | 0.8% |

Has your organisation experienced supply chain shortages as a result of the conflict in the Middle East? (900 respondents)

| No | 79.8% |

| Yes | 20.2% |

To what extent has your organisation been negatively impacted by supply chain shortages as a result of the conflict in the Middle East? (182 respondents – those that have experienced shortages)

| No impact | 1.1% |

| To a slight extent | 66.5% |

| To a significant extent | 32.4% |

Has your organisation been impacted by any of the following key shortages? Please select all that apply. (182 respondents – those that have experienced shortages)

| Fuel or energy (e.g. diesel, gas, electricity) | 55.5% |

| Industrial materials (e.g. plastics, chemicals, metals) | 38.5% |

| Components or parts (e.g. electronics, machinery) | 33.5% |

| Other | 13.2% |

| Construction materials | 12.1% |

| Food or agricultural inputs, including fertilisers and animal feed | 7.1% |

| Medicines or medical supplies | 5.5% |

Are you worried about shortages impacting your business in the coming months? (883 respondents)

| No | 47.7% |

| Yes | 52.3% |

In which of the following inputs, if any, are you most concerned you will suffer shortages? Please select all that apply. (471 respondents – those that are worried about shortages)

| Fuel or energy (e.g. diesel, gas, electricity) | 75.8% |

| Components or parts (e.g. electronics, machinery) | 34.8% |

| Industrial materials (e.g. plastics, chemicals, metals) | 33.8% |

| Construction materials | 18.9% |

| Food or agricultural inputs, including fertilisers and animal feed | 15.7% |

| Medicines or medical supplies | 9.8% |

| Other | 7.9% |

Have you taken, or are you planning to take, action to mitigate the impact of shortages on your business? (883 respondents)

| None | 36.9% |

| Increased awareness of supply chains | 25.3% |

| Improved relationships with key suppliers | 18.6% |

| Diversification of suppliers across a broader range of countries | 18.4% |

| Stockpiling and surge capacity | 14.4% |

| Demand management | 13.9% |

| Not sure | 10.4% |

| Onshoring | 5.2% |

| Relocated existing sourcing to another country | 5.2% |

| Other | 4.9% |